29. Stock Exchange

In this chapter, we design an electronic stock exchange system.

The basic function of an exchange is to facilitate the matching of buyers and sellers efficiently. This fundamental function has not changed over time. Before the rise of computing, people exchanged tangible goods by bartering and shouting at each other to get matched. Today, orders are processed silently by supercomputers, and people trade not only for the exchange of products, but also for speculation and arbitrage. Technology has greatly changed the landscape of trading and exponentially boosted electronic market trading volume.

When it comes to stock exchanges, most people think about major market players like The New York Stock Exchange (NYSE) or Nasdaq, which have existed for over fifty years. In fact, there are many other types of exchange. Some focus on vertical segmentation of the financial industry and place special focus on technology [1], while others have an emphasis on fairness [2]. Before diving into the design, it is important to check with the interviewer about the scale and the important characteristics of the exchange in question.

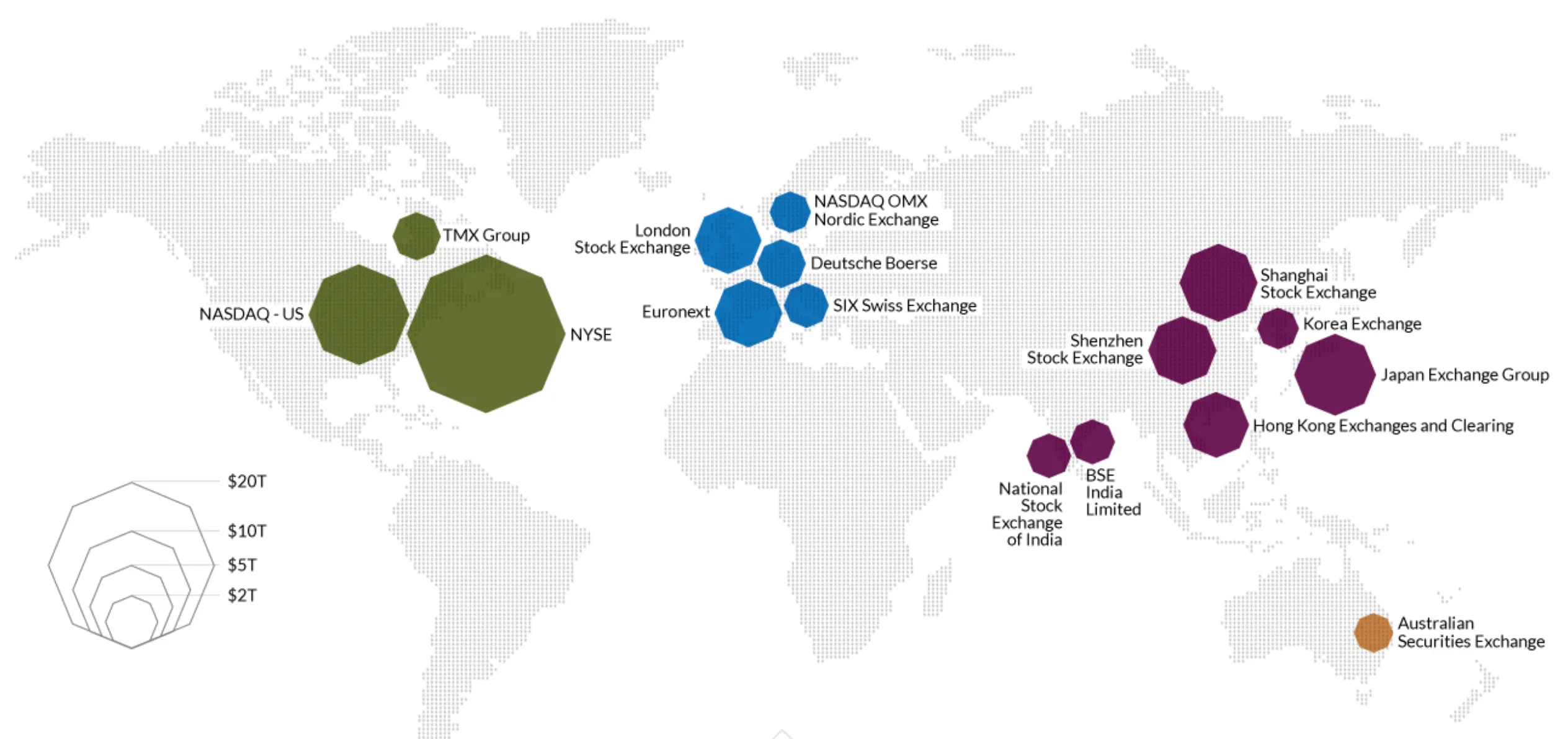

Just to get a taste of the kind of problem we are dealing with; NYSE is trading billions of matches per day [3], and HKEX about 200 billion shares per day [4]. Figure 1 shows the big exchanges in the “trillion-dollar club” by market capitalization.

Figure 1 Largest stock exchanges (Source: [5])

Figure 1 Largest stock exchanges (Source: [5])

Step 1 - Understand the Problem and Establish Design scope

A modern exchange is a complicated system with stringent requirements on latency, throughput, and robustness. Before we start, let’s ask the interviewer a few questions to clarify the requirements.

Candidate: Which securities are we going to trade? Stocks, options, or futures?

Interviewer: For simplicity, only stocks.

Candidate: Which types of order operations are supported: placing a new order, canceling an order, or replacing an order? Do we need to support limit order, market order, or conditional order?

Interviewer: We need to support the following: placing a new order and canceling an order. For the order type, we only need to consider the limit order.

Candidate: Does the system need to support after-hours trading?

Interviewer: No, we just need to support the normal trading hours.

Candidate: Could you describe the basic functions of the exchange? And the scale of the exchange, such as how many users, how many symbols, and how many orders?

Interviewer: A client can place new limit orders or cancel them, and receive matched trades in real-time. A client can view the real-time order book (the list of buy and sell orders). The exchange needs to support at least tens of thousands of users trading at the same time, and it needs to support at least 100 symbols. For the trading volume, we should support billions of orders per day. Also, the exchange is a regulated facility, so we need to make sure it runs risk checks.

Candidate: Could you please elaborate on risk checks?

Interviewer: Let’s just do simple risk checks. For example, a user can only trade a maximum of 1 million shares of Apple stock in one day.

Candidate: I noticed you didn’t mention user wallet management. Is it something we also need to consider?

Interviewer: Good catch! We need to make sure users have sufficient funds when they place orders. If an order is waiting in the order book to be filled, the funds required for the order need to be withheld to prevent overspending.

Non-functional requirements

After checking with the interviewer for the functional requirements, we should determine the non-functional requirements. In fact, requirements like “at least 100 symbols” and “tens of thousands of users” tell us that the interviewer wants us to design a small-to-medium scale exchange. On top of this, we should make sure the design can be extended to support more symbols and users. Many interviewers focus on extensibility as an area for follow-up questions.

Here is a list of non-functional requirements:

-

Availability. At least 99.99%. Availability is crucial for exchanges. Downtime, even seconds, can harm reputation.

-

Fault tolerance. Fault tolerance and a fast recovery mechanism are needed to limit the impact of a production incident.

-

Latency. The round-trip latency should be at the millisecond level, with a particular focus on the 99th percentile latency. The round trip latency is measured from the moment a market order enters the exchange to the point where the market order returns as a filled execution. A persistently high 99th percentile latency causes a terrible user experience for a small number of users.

-

Security. The exchange should have an account management system. For legal compliance, the exchange performs a KYC (Know Your Client) check to verify a user’s identity before a new account is opened. For public resources, such as web pages containing market data, we should prevent distributed denial-of-service (DDoS) [6] attacks.

Back-of-the-envelope estimation

Let’s do some simple back-of-the-envelope calculations to understand the scale of the system:

- 100 symbols

- 1 billion orders per day

- NYSE Stock Exchange is open Monday through Friday from 9:30 am to 4:00 pm Eastern Time. That’s 6.5 hours in total.

- QPS: 1 billion / 6.5 / 3600 = ~43,000

- Peak QPS: 5 * QPS = 215,000. The trading volume is significantly higher when the market first opens in the morning and before it closes in the afternoon.

Step 2 - Propose High-Level Design and Get Buy-In

Before we dive into the high-level design, let’s briefly discuss some basic concepts and terminology that are helpful for designing an exchange.

Business Knowledge 101

Broker

Most retail clients trade with an exchange via a broker. Some brokers whom you might be familiar with include Charles Schwab, Robinhood, Etrade, Fidelity, etc. These brokers provide a friendly user interface for retail users to place trades and view market data.

Institutional client

Institutional clients trade in large volumes using specialized trading software. Different institutional clients operate with different requirements. For example, pension funds aim for a stable income. They trade infrequently, but when they do trade, the volume is large. They need features like order splitting to minimize the market impact [7] of their sizable orders. Some hedge funds specialize in market making and earn income via commission rebates. They need low latency trading abilities, so obviously they cannot simply view market data on a web page or a mobile app, as retail clients do.

Limit order

A limit order is a buy or sell order with a fixed price. It might not find a match immediately, or it might just be partially matched.

Market order

A market order doesn�’t specify a price. It is executed at the prevailing market price immediately. A market order sacrifices cost in order to guarantee execution. It is useful in certain fast-moving market conditions.

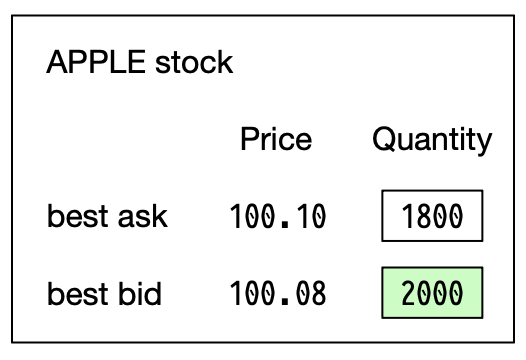

Market data levels

The US stock market has three tiers of price quotes: L1 (level 1), L2, and L3. L1 market data contains the best bid price, ask price, and quantities (Figure 2). Bid price refers to the highest price a buyer is willing to pay for a stock. Ask price refers to the lowest price a seller is willing to sell the stock.

Market data levels

The US stock market has three tiers of price quotes: L1 (level 1), L2, and L3. L1 market data contains the best bid price, ask price, and quantities (Figure 2). Bid price refers to the highest price a buyer is willing to pay for a stock. Ask price refers to the lowest price a seller is willing to sell the stock.

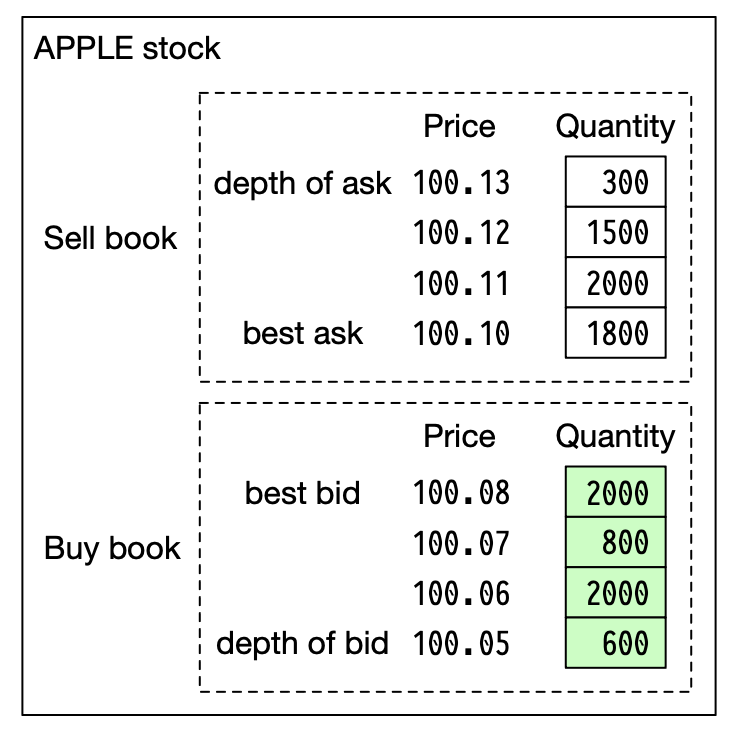

L2 includes more price levels than L1 (Figure 3).

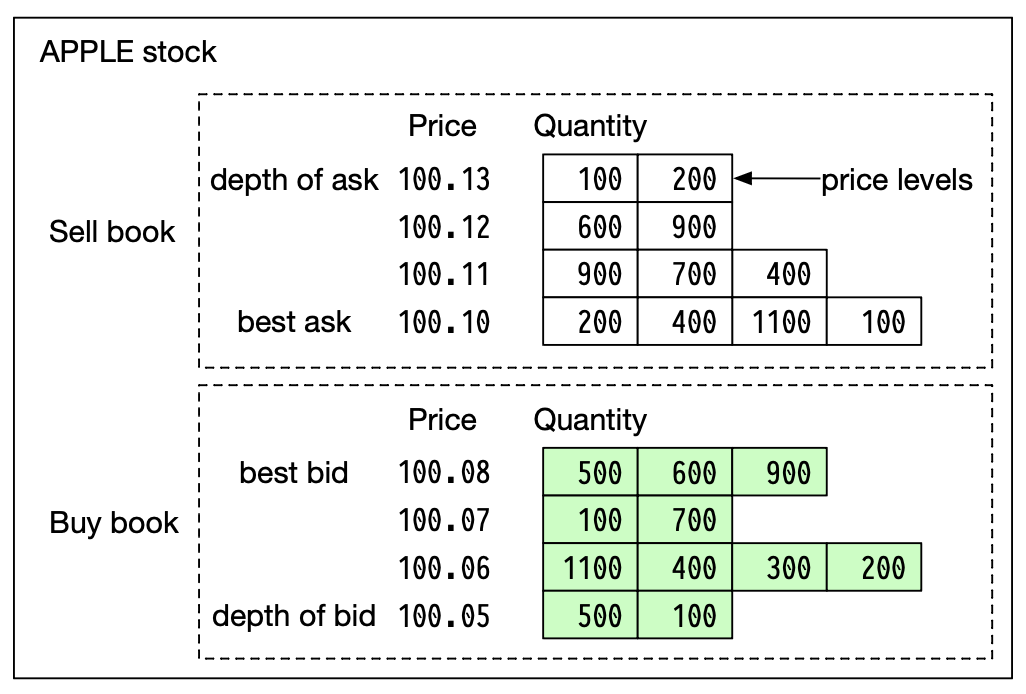

L3 shows price levels and the queued quantity at each price level (Figure 4).